The Tally Newsletter, Issue 48

October 14, 2021

Welcome back for issue 48 of the Tally Newsletter, a publication focused on all things decentralized governance. We’ll keep you updated on key proposals, procedural changes, newly launched voting systems, shifting power dynamics, and anything else you need to know to be an informed citizen.

This week we cover:

MakerDAO Considering a Shift to Zero Fee Stablecoin Trading

Sybil Attack on Ribbon Airdrop Leads to Review of Prior Token Distributions

Plus some brief ecosystem updates.

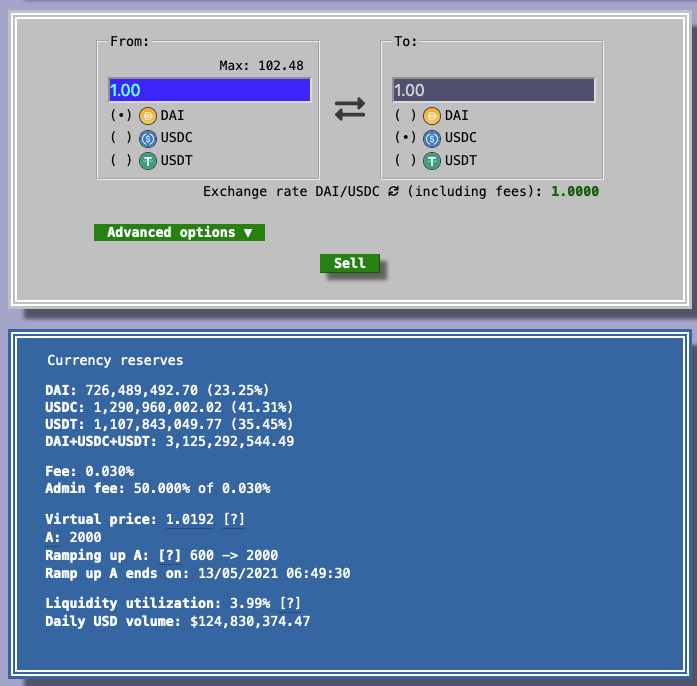

MakerDAO Votes on Eliminating Stablecoin Trading Fees

TL;DR: Reducing the fee parameters for Maker’s Peg Stability Module should strengthen the DAI<>USD peg, but could also have unpredictable impacts on other defi platforms and asset flows.

MakerDAO is considering an initial proposal to reduce stablecoin trading fees to zero. With the current Peg Stability Module (PSM) parameters, trading from DAI to another supported stablecoin such as USDC or USDP is free, but a fee of between 0.1 to 0.2% is charged for those trading from an external stablecoin into DAI. This effectively manages DAI’s peg against fiat stablecoins (and therefore USD price) between $1 and $1.001.

Source: Coingecko DAI Chart

While this narrow trading range is a substantial improvement over 2020 price dynamics, where DAI frequently traded several percent above the peg, it still causes challenges for DAI adoption and integration. As an example, a 0.1% trading fee between DAI and USD leads to a nearly 0.5% increase in annualized borrowing costs for a 3 month loan. Additionally, many centralized trading platforms and OTC desks consider DAI as a volatile currency instead of a fully exchangeable stablecoin, which leads to worse execution and higher costs for users. These challenges together make DAI far less appealing, particularly those in the real world asset lending industry.

Source: Curve 3pool

Reducing the fees to zero as proposed would lead to significant changes in DAI usage and the wider stablecoin and defi markets. Full exchangeability will drive inflows into the PSM to equalize DAI price throughout the market. Looking at Curve Finance and other decentralized exchange platforms, there is over $200-300 million in liquidity available to sell DAI above $1 (equalizing the quantity of DAI versus other stablecoins within liquidity pools), which should be immediately utilized through arbitrage transactions. Including markets on centralized exchanges and additional defi platforms, inflows of USDC and Paxos Dollar could easily reach over $1 billion.

With Maker offering no fee stablecoin swaps, this could also draw trading volume away from decentralized exchange platforms such as Curve and Uniswap. This would counteract Maker’s planned transition from direct stablecoin holdings to indirect holdings through liquidity pool tokens such as the G-UNI-DAI-USDC vault. In summary, removing PSM trading fees would make MakerDAO more vulnerable to targeted blacklisting by fiat stablecoin issuers, with an increase in direct exposure and reduction of potentially viable alternatives.

While PSM fee reductions are likely to increase DAI supply, it could have unpredictable impact on DAI demand. Nearly 1 billion DAI is currently deposited within automated market maker liquidity pools such as Curve and Uniswap. Undercutting these platform’s fees could reduce demand for DAI due to fewer available options for earning passive yield.

Source: MakerDAO Forum

So far, these concerns don’t seem to have dissuaded many community members. The forum poll is live until Monday October 25, and if passed in the forum and through subsequent on-chain voting, it would mark a significant change in Maker’s stablecoin strategy. Instead of externalizing stablecoin holdings into other protocols like Curve and Uniswap, Maker will need to focus on real world assets and credit investments beyond the crypto ecosystem.

Community Members Uncover Sybil Attacks in a Range of Defi Airdrops

TL;DR: While the Ribbon Finance distribution was remediated, newly uncovered incidents call into question the viability of retroactive airdrops more generally.

Ribbon Finance, a protocol for structured products and sustainable yield generation, recently enabled governance with a distribution of RBN tokens to past protocol users. Since Uniswap’s token launch last year, retroactive user distributions have formed a key part of token launch mechanisms, helping to reward early adopters and bootstrap a financially aligned community from day one. But recent events in the RBN distribution question the viability of these airdrops going forward.

Shortly after Ribbon Finance enabled transferability of their RBN governance token, some community members noticed unusual trading activity that led to uncovering a large-scale sybil attack on the token distribution.

After reviewing transaction data, it became clear that certain sybil accounts led back to Divergence Ventures, a private investor in Ribbon who may have had access to non-public information about the airdrop mechanism.

Over the following day, Divergence was pressured to return the airdropped funds as well as donate their investment holdings to a non profit organization, leaving them with no remaining ownership of the Ribbon protocol. Additional recipients also returned airdropped funds to resolve potential conflicts of interest:

As the Ribbon Finance drama began to abate after funds were returned, researchers’ attention passed to other projects with similar retroactive airdrops that rewarded funds on a per address basis. These include the FORTH and DYDX airdrops among several other projects.

All of these compromised drops shared a common feature of giving sub-linear returns based on amount of capital committed - this allows single parties to earn a higher share of rewards by splitting their funds into small pieces to appear like many independent users. Protocols typically target drops in this way because it decentralizes governance power among many community members quickly. But the ability to game the distribution, particularly with private information, creates substantial risk.

As a result of these uncovered issues, projects may need to revisit their token distribution plans. This could include a reduced focus on per account rewards, along with better screening for sybil accounts and changes in investor communication practices to avoid sharing sensitive information.

SEC releases comments on funds holding Bitcoin futures, deepening speculation on a potential Bitcoin ETF approval:

Indexed Finance suffers from exploits on DEFI5 and CC10 indexes:

Uniswap funded Defi Education Fund considers moving assets to centralized custodian:

Compound proposal 65 resolves last outstanding issues from rewards bug:

Tyler Loewen@tyleretherCompound Proposal 65 introduces a one-off function to correct over-accrued COMP, called through a governance proposal containing verifiable data. Once executed, it will correct all over-accrued COMP and restore COMP claiming functionality for all users.10:48 PM · Oct 11, 20213 Likes

Tyler Loewen@tyleretherCompound Proposal 65 introduces a one-off function to correct over-accrued COMP, called through a governance proposal containing verifiable data. Once executed, it will correct all over-accrued COMP and restore COMP claiming functionality for all users.10:48 PM · Oct 11, 20213 Likes

Thanks for joining us for issue 48 of the Tally Newsletter. Be sure to check out the Tally governance app and join us on Discord for the latest updates!

Anything we missed? New developments or protocols you’d like to see covered? Drop us a line at newsletter@withtally.com

Best,

Nate, Tally